About Me

Hi, I'm Rita.

I'm a Mortgage Professional with broad experience in all aspects of the financing process - whether it be helping first-time buyers purchase their first home; assisting clients with financing for a renovation to their existing home; building a new home or helping them re-negotiate their mortgage at renewal.

My goal is to help my clients navigate through the process of finding the right financing product for their unique situation.

I specialize in mortgages for self-employed borrowers; borrowers with slightly bruised credit and first time home buyers, home equity Lines of Credit; first & second mortgages; mortgage renewals; re-finances and investment property mortgages.

Cell: 403-502-3330

STEP ONE

Start the conversation.

The best place to start is to connect with me directly. The mortgage process is personal, and it can be daunting. My commitment to you is that I'll listen to all your needs, assess your financial situation, and provide you with a plan to move forward.

STEP TWO

Choose the best option.

Once we’ve had a look at your financial situation, we’ll consider a variety of mortgage options, I’ll outline what documents are necessary to qualify for a mortgage, negotiate with the lenders on your behalf, and arrange the mortgage that best suits your needs.

STEP THREE

Sit back and relax.

Once we’ve arranged the mortgage product that best suits your needs, you’re not alone. I’m your mortgage professional for life. If you’ve got questions in the years to come, I’m always available to make sure that your mortgage is working for you, and not the other way around!

Lenders

I've developed excellent relationships with many lenders across the country.

Let's figure out which one has the best product for you.

Services

As a mortgage professional it's my job to be the go-between between you and a mortgage lender. I make sure that you know all the products available to you, and are equipped with the knowledge to make the best decisions for you and your family.

Flexible Mortgages

As your life can change at any time, I offer a wide range of flexible mortgage products.

Qualified Advice

As a licensed mortgage expert, I'll listen to your needs and answer your questions.

No Cost to You

There are no fees for my services, once you find the perfect product, the lender pays me a commission.

Advocacy

I commit to working on your behalf

to find you the best mortgage for your needs.

Mortgage Articles

The best place to start the mortgage process is with a pre-approval. But once you’ve been pre-approved for a mortgage and you’ve been shopping with location in mind, what happens when you can’t find a suitable property? There's no doubt about it; finding the perfect property within your price range is a difficult task, especially for first-time homebuyers. So, before buyer’s fatigue sets in, maybe you should consider adding the cost of renovations into your purchase. Buying a property and including the cost of renovations into the mortgage is available through a program called purchase plus improvements. When purchasing a home, you can add the cost of home upgrades into your mortgage, making it a great option if you can’t find something move-in ready and aren’t afraid to do a little work! But while this sounds simple enough, in all honestly, it’s quite the process. There are some pretty strict rules to follow, but nothing that you can’t handle with the guidance of an independent mortgage professional. Here’s a quick overview of the process. Firstly, you must provide quotes to the lender ahead of time for the work you would like to complete. It’s good to note that the renovations will have to increase the value of the property accordingly. From there, the lender doesn’t give you the money to do the upgrades; you have to come up with that yourself. However, once the work has been completed and verified by an appraiser, the lender will reimburse you and include the money in your mortgage. This program isn’t for everyone. Buying a home is a stressful endeavour in and of itself. The added stress of having to undertake renovations right away might not be a good idea. But then again, if you have the financial wherewithal to handle the cost of renovations and like the idea of making it yours from the start, then this might be just the option you’ve been looking for! Please connect directly; it would be a pleasure to walk through the exact process and outline what securing a purchase plus improvements would look like for you!

If you’ve missed a payment on your credit card or line of credit and you’re wondering how to handle things and if this will impact your creditworthiness down the road, this article is for you. But before we get started, if you have an overdue balance on any of your credit cards at this exact moment, go, make the minimum payment right now. Seriously, log in to your internet banking and make the minimum payment. The rest can wait. Here’s the good news, if you’ve just missed a payment by a couple of days, you have nothing to worry about. Credit reporting agencies only record when you’ve been 30, 60, and 90 days late on a payment. So, if you got busy and missed your minimum payment due date but made the payment as soon as you realized your error, as long as you haven’t been over 30 days late, it shouldn’t show up as a blemish on your credit report. However, there’s nothing wrong with making sure. You can always call your credit card company and let them know what happened. Let them know that you missed the payment but that you paid it as soon as you could. Keeping in contact with them is the key. By giving them a quick call, if you have a history of timely payments, they might even go ahead and refund the interest that accumulated on the missed payment. You never know unless you ask! Now, if you’re having some cash flow issues, and you’ve been 30, 60, or 90 days late on payments, and you haven’t made the minimum payment, your creditworthiness has probably taken a hit. The best thing you can do is make all the minimum payments on your accounts as soon as possible. Getting up to date as quickly as possible will mitigate the damage to your credit score. The worst thing you can do is bury your head in the sand and ignore the problem, because it won’t go away. If you cannot make your payments, the best action plan is to contact your lender regularly until you can. They want to work with you! The last thing they want is radio silence on your end. If they haven’t heard from you after repeated missed payments, they might write off your balance as “bad debt” and assign it to a collection agency. Collections and bad debts look bad on your credit report. As far as qualifying for a mortgage goes, repeated missed payments will negatively impact your ability to get a mortgage. But once you’re back to making regular payments, the more time that goes by, the better your credit will get. It’s all about timing. Always try to be as current as possible with your payments. So If you plan to buy a property in the next couple of years, it’s never too early to work through your financing, especially if you’ve missed a payment or two in the last couple of years and you’re unsure of where you stand with your credit. Please connect directly; it would be a pleasure to walk through your mortgage application and credit report. Let’s look and see exactly where you stand and what steps you need to take to qualify for a mortgage.

Refinancing your mortgage can be a smart financial move, but how do you know if it’s the right time? Whether you’re looking to lower your monthly payments, access home equity, or consolidate debt, refinancing can offer valuable benefits. Here are five key signs that it might be the right time to refinance your mortgage in Canada. 1. Interest Rates Have Dropped One of the most common reasons Canadians refinance is to secure a lower interest rate. Even a small decrease in your mortgage rate can lead to significant savings over time. If rates have dropped since you took out your mortgage, refinancing could help you reduce your monthly payments and save thousands in interest. ✅ Tip: Check with your mortgage broker to compare your current rate with today’s market rates. 2. Your Financial Situation Has Improved If your credit score has increased or your income has stabilized since you first got your mortgage, you might qualify for better loan terms. Lenders offer lower rates and better conditions to borrowers with strong financial profiles. ✅ Tip: If you’ve paid off debts, improved your credit score, or increased your savings, refinancing could work in your favour. 3. You Want to Consolidate High-Interest Debt Carrying high-interest debt from credit cards, personal loans, or lines of credit? Refinancing can help consolidate those debts into your mortgage at a much lower interest rate. This can make monthly payments more manageable and reduce the overall cost of borrowing. ✅ Tip: Make sure the savings from refinancing outweigh any prepayment penalties or fees. 4. You Need to Free Up Cash for a Major Expense Many Canadians refinance to access their home’s equity for renovations, education costs, or major life expenses. With home values rising in many areas, a refinance could help you tap into that value while still keeping manageable payments. ✅ Tip: Consider a home equity line of credit (HELOC) if you need flexible access to funds. 5. Your Mortgage Term is Ending, and You Want Better Terms If your mortgage is up for renewal, it’s the perfect time to explore refinancing options. Instead of simply accepting your lender’s renewal offer, compare rates and terms to see if you can get a better deal elsewhere. ✅ Tip: A mortgage broker can help you shop around and negotiate better terms on your behalf. Is Refinancing Right for You? Refinancing isn’t always the best move—there can be penalties for breaking your current mortgage, and not all savings are worth the switch. However, if you relate to any of the five signs above, it’s worth discussing your options with a mortgage professional. Thinking about refinancing? Let’s chat and find the best option for you!

Nice things people have said about working with me.

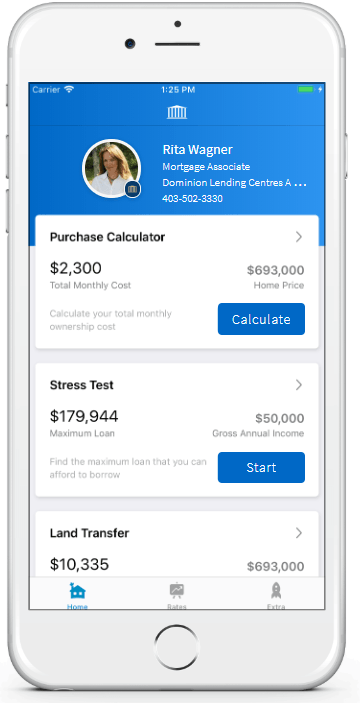

Download My Mortgage Toolbox

WHAT CAN YOU DO WITH MY APP

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese