About Me

Hi, I'm Rita.

I'm a Mortgage Professional with broad experience in all aspects of the financing process - whether it be helping first-time buyers purchase their first home; assisting clients with financing for a renovation to their existing home; building a new home or helping them re-negotiate their mortgage at renewal.

My goal is to help my clients navigate through the process of finding the right financing product for their unique situation.

I specialize in mortgages for self-employed borrowers; borrowers with slightly bruised credit and first time home buyers, home equity Lines of Credit; first & second mortgages; mortgage renewals; re-finances and investment property mortgages.

Cell: 403-502-3330

STEP ONE

Start the conversation.

The best place to start is to connect with me directly. The mortgage process is personal, and it can be daunting. My commitment to you is that I'll listen to all your needs, assess your financial situation, and provide you with a plan to move forward.

STEP TWO

Choose the best option.

Once we’ve had a look at your financial situation, we’ll consider a variety of mortgage options, I’ll outline what documents are necessary to qualify for a mortgage, negotiate with the lenders on your behalf, and arrange the mortgage that best suits your needs.

STEP THREE

Sit back and relax.

Once we’ve arranged the mortgage product that best suits your needs, you’re not alone. I’m your mortgage professional for life. If you’ve got questions in the years to come, I’m always available to make sure that your mortgage is working for you, and not the other way around!

Lenders

I've developed excellent relationships with many lenders across the country.

Let's figure out which one has the best product for you.

Services

As a mortgage professional it's my job to be the go-between between you and a mortgage lender. I make sure that you know all the products available to you, and are equipped with the knowledge to make the best decisions for you and your family.

Flexible Mortgages

As your life can change at any time, I offer a wide range of flexible mortgage products.

Qualified Advice

As a licensed mortgage expert, I'll listen to your needs and answer your questions.

No Cost to You

There are no fees for my services, once you find the perfect product, the lender pays me a commission.

Advocacy

I commit to working on your behalf

to find you the best mortgage for your needs.

Mortgage Articles

Why Work With an Independent Mortgage Professional? If you’re in the market for a mortgage, here’s the most important thing to know: Working with an independent mortgage professional can save you money and provide better options than dealing directly with a single bank. If that’s all you read—great! But if you’d like to understand why that statement is true, keep reading. The Best Mortgage Isn’t Just About the Lowest Rate It’s easy to fall for slick marketing that promotes ultra-low mortgage rates. But the lowest rate doesn’t always mean the lowest cost . The best mortgage is the one that costs you the least amount of money over time —not just the one with the flashiest headline rate. Things like: Prepayment penalties Portability Flexibility to refinance Amortization structure Fixed vs. variable terms …can all affect the true cost of your mortgage. An independent mortgage professional looks beyond the rate. They’ll help you find a product that fits your unique financial situation , long-term goals, and lifestyle—so you’re not hit with expensive surprises down the road. Save Time (and Your Sanity) Applying for a mortgage can be complicated. Every lender has different rules, documents, and policies—and trying to navigate them all on your own can be time-consuming and frustrating. When you work with an independent mortgage professional: You fill out one application They shop that application across multiple lenders You get expert advice tailored to your needs This means less paperwork , less stress , and more confidence in your options. Get Unbiased Advice That Puts You First Bank specialists work for the bank. Their job is to sell you that bank’s mortgage products—whether or not it’s the best deal for you. Independent mortgage professionals work for you. They’re provincially licensed, and their job is to help you: Compare multiple lenders Understand the fine print Make informed, long-term financial decisions And the best part? Their services are typically free to you . Mortgage professionals are paid a standardized fee by the lender when a mortgage is placed—so you get expert guidance without any out-of-pocket cost. Access More Mortgage Options When you go to your bank, you’re limited to that bank’s mortgage products. When you go to an independent mortgage professional, you get access to: Major banks Credit unions Monoline lenders (who only offer mortgages) Alternative and private lenders (if needed) That’s far more choice , and a much better chance of finding a mortgage that truly fits your needs and goals. The Bottom Line If you want to: Save money over the life of your mortgage Save time by avoiding unnecessary back-and-forth Access more lenders and products Get honest, client-first advice …then working with an independent mortgage professional is one of the smartest decisions you can make. Let’s Make a Plan That Works for You If you're ready to talk about mortgage financing—or just want to explore your options—I'm here to help. Let's connect and put together a strategy that makes sense for your goals and your future. Reach out anytime. I’d be happy to help.

Buying a Home? Follow These 6 Key Steps for a Smooth Experience Buying a home is likely one of the biggest financial decisions you’ll ever make. It’s exciting—but it can also be overwhelming, especially when it comes to understanding how mortgage financing works. To help make the process smoother (and far less stressful), here are six essential steps every homebuyer should follow: 1. Start With a Mortgage Professional—Not MLS It’s tempting to start your home search by scrolling through listings and booking showings—but the real first step should be speaking with an independent mortgage professional . Unlike a bank that offers only one set of products, an independent mortgage expert has access to multiple lenders and options . That means better advice, better rates, and a better chance of finding a mortgage that truly fits your needs. 2. Build a Personalized Mortgage Plan Unless you’re buying your home with cash, you’ll need a solid financing strategy. That means: Reviewing your credit score Running affordability calculations Exploring different mortgage types, terms, and features Understanding down payments and closing costs The sooner you start planning, the more confident you’ll feel. Don’t wait until you’ve found the “perfect” property— get ahead of the process now . 3. Figure Out What You Can Actually Afford What a lender says you can borrow doesn’t always match what you can comfortably pay each month. Take a close look at your budget, lifestyle, and spending habits. Think about how your mortgage payments, property taxes, utilities, and other costs will fit into your everyday cash flow. Avoid the stress of being house-poor by knowing your real-life affordability , not just your paper pre-approval. 4. Get Pre-Approved the Right Way A true mortgage pre-approval isn’t just entering numbers into an online calculator. It means: Completing a mortgage application Submitting all your required documentation Having a mortgage professional fully assess your file When you’re officially pre-approved, you’ll shop for homes with confidence , knowing what you qualify for and that you’re financially ready. 5. Submit Your Documents Promptly and Stay Flexible Once you find a property and your offer is accepted, time is of the essence. That’s when all the upfront work you’ve done really pays off. Be ready to: Provide additional documentation if requested Respond to your mortgage professional quickly Stay flexible and proactive throughout the approval process Your lender needs to verify everything before finalizing the loan, so staying organized is key. 6. Don’t Make Big Financial Changes Before Closing Once you’ve secured financing and waived your conditions, freeze your finances until after you get the keys. Seriously—don’t: Change jobs Apply for new credit Take out a loan Make a large withdrawal Even small changes can throw off your approval. Keep everything status quo until you officially take possession. Recap: 6 Steps to a Smooth Home Purchase Connect with an independent mortgage professional Create a mortgage plan early Know what you can afford (not just what you qualify for) Get fully pre-approved Stay on top of documentation Avoid major financial changes before possession Ready to Buy with Confidence? If you’re thinking about buying a home—or just want to know what’s possible—let’s talk. I’ll help you map out a personalized plan that makes your homebuying journey feel simple, strategic, and stress-free. Reach out anytime. I’d love to help you get started.

The Bank of Canada announced today that it is holding its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. The tone of today's announcement is notably more optimistic than previous months. Here's what's changed and what it means for you.

Nice things people have said about working with me.

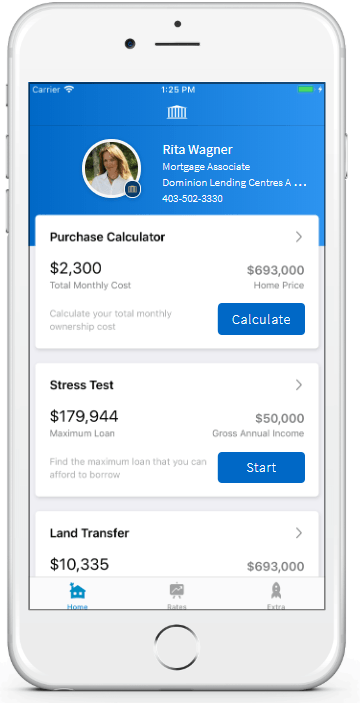

Download My Mortgage Toolbox

WHAT CAN YOU DO WITH MY APP

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese